Message from Chairman Desk

Office Bearers

CA. Manish Gadia

Chairman

CA. Drushti Desai

Vice Chairperson

CA. Arpit Kabra

Secretary

CA. Jayesh Kala

Treasurer

Editorial Board

CA. Manish Gadia

CA. Drushti Desai

CA. Arpit Kabra

CA. Jayesh Kala

CA. Lalit Bajaj

CA. Murtuza Kachwala

CA. Priti Savla Ex-Officio

CA. Prafulla Chhajed

Dear Professional Colleagues,

“Dream is not what you see in sleep, Dream is something which doesn’t let you sleep”

This quote by our beloved past president of India Dr. A.P.J. Abdul Kalam inspires us to dream big. Dreams transform into thoughts and thoughts result in action. Dreams are the seeds of change. Nothing ever grows without a seed and nothing ever changes without a dream.

Initiatives for Women CA Members

Khoj

I am pleased to state that ‘Khoj’ – A woman empowerment initiative will look to provide opportunities for job placement or assignments to Women CAs with CA firms across the Western Region of ICAI.

https://wirc-icai.org/women-empowerment-job-portal/

CA Women Faculties Invitation

Education is the foundation of our success. To encourage CA Women members to spread knowledge as faculty for the new generation we have invited applications from them and look forward to an enthusiastic response.

CA women members who wish to become faculty, kindly click on the link below & register yourself https://forms.gle/mqXTNaosFApncm1G8

Mentorship Program: Connect-Learn-Grow

Under this program, members can get assistance from experts in the field through on the jobmentorship or through periodic assistance in various areas related topractice or industry on regular basis through online or offline mode from the veterans of our profession. This initiative of WIRC will accelerate thegrowth of young CA’s and will lead totheir all-round development.

https://wirc-icai.org/mentorship-portal/

CFO Forum

We will form a forum of CFOs of large companies, wherethey will meet and discuss on a pre-decided topic and share their experience. This will be an excellent platform to share knowledge as well as network among industry leaders.

Requesting you to click this link and complete your details.

CEO Speak – “Journey from CA to CEO”

Chartered Accountants have the drive to learn and grow due to the training in our formative years. Many CAs have reached great heights in the course of their professional lives and we feel that such motivating accounts must be communicated to the world at large. Hence, ‘CEO Speak’ will highlight the inspiring trials and successes of fellow CAs to the fraternity at large.

Members Meet

The Members Meet saw ICAI President CA. Nihar Jambusaria, ICAI Vice President CA. (Dr.) Debashis Mitra and WIRC Office Bearers interact with a host of Past Presidents. We were proud to interact with ICAI Past Presidents like CA. N.P. Sarda, CA. Y.M. Kale, CA. M.M. Chitale, CA. Sunil H. Talati, CA. Kamlesh Vikamsey, CA. Nilesh Vikamsey and CA. Prafulla Chhajed.

TEL - Train, Earn, Learn Initiative

In these times, it is vital we find ways to support the future of the profession. WIRC is proud to commence the TEL model where college students get direct training and actual work experience at CA firms. Thus, enabling them to earn and learn, and creating a supportive environment for our students.

Charitable Trust Clinic

Section 12 AB has been introduced in Income Tax Act, 1961, where all the charitable entities need to re-register before 30th June, 2021. As professionals we receive many queries regarding same. To provide guidance to the members, WIRC has created a virtual clinic on its website where members can send their queries which will be answered by a panel of experts.

Long Duration Course on Technology

Technology has taken over our lives and the profession. We are more efficient and faster with the help of technology andour reliance will surely increase in the future.In order to be future-ready we have planned to commence a long duration course on technology for the betterment of the profession.

Short Videos of Updates

Today the world has moved to the screen for personal & professional interaction and for education. Keeping up with the times, WIRC has created and will continue to create short videos of updates such as GST, and other technical topics by expert members. These short but highly informative videos are uploaded on YouTube to provide all our members free access to information and updates. For viewing these updates members can subscribe to WIRC YouTube channel.

https://www.youtube.com/channel/UCYMoI6owwVEKk90_y2_YWvQ/videos

WIRC Wellness Series

Looking at the current scenario, we can agree that health is indeed wealth. However, we need better and clearer information on taking care of ourselves and family members. To that end, WIRC will be conducting a series of lectures focused on wellness. I request all members to take advantage of this unique series organised for the fraternity.

Meals at Doorsteps

Many of our members are in quarantine. To assist their families and help them during the lockdown, WIRC has arranged to supply meals for Covid Quarantined CA family members. We are confident that this measure will provide relief to stressed families and look forward to increasing its scope.

Let us remember and be encouraged by these inspiring words, “Let your dreams be bigger than your fears, your actions louder than your words and your faith stronger than your feelings.”

I request you to share your ideas, vision and suggestions to wirc@icai.in

As always, take care, stay safe and remain healthy.

CA. Manish Gadia

Chairman

Report on Branch Activities

Dear professional colleagues,

This is a corner where we report the activities undertaken by the Branches in Western Region under the various initiatives undertaken by them. We conducted during the month branch orientation on virtual mode where all the President CA Nihar Jambusaria and Vice President CA (Dr.) Debashish Mitra addressed all the branches. We also learnt about the ongoing and proposed activities of the branches.

In current times all of us are facing issues either on personal front or on professional front. Despite all of this we have risen above our personal engagements to serve our fraternity and the society. The Branches of the Region have risen to the need of the hour and have served the society in various ways.

Ahmedabad Branch has rolled out a fitness program called FIT 73. 43 branches of ICAI pan India have joined this initiative. Over 2000 participants across india have become members of this movement. It has conducted Plasma donation camp and also laid out taxi service for COVID patients to commute to healthcare facility.

Blood donation camps have been rolled out by Ahmedabad, Ahmednagar, Amravati and Solapur Branch.

Satara and Surat Branch have set up Oxygen concentrators service for members.

Members of Navsari Branch contributed to set up an oxygen plant.

Members of Morbi CPE Chapter have come together and contributed an ambulance.

Bhuj Branch has donated a dialysis machine to Bhuj Lions Hospital.

Further, Ahmedabad and Solapur Branch have also distributed meals to COVID affected families.

Pune branch has tied up with PCMC for easy donation of blood and plasma whereby the samples for the same will be collected from the donor’s home and then appointment will be given to go to the centre for donation.

Kalyan Dombivali Branch carried out awareness programs for COVID and also distributed food kits amongst needy.

Thane, Nagpur Branch have set up COVID task force. Sangli Branch formed a whatsapp group for helpdesk for plasma.

Nagpur Branch has also tied up for RT PCR test and HRCT at discounted rate for members as also created a COVID awareness banner.

Baroda Branch has collated all the relevant data about facilities for COVID.

Surat, Ahmedabad, Anand have continued Vaccination drives.

CA. Drushti Desai

Vice Chairperson

Forthcoming Events : Webinar for Members

|

04-05-2021

Tuesday to 09-05-2021 Sunday |

6.00 p.m. to 9.00 p.m. ₹ 2950/- (Incl. GST) |

Virtual Workshop on Excel Skill for Business |

|

04-05-2021 Tuesday |

5.00 p.m. to 7.00 p.m. ₹ 236/- (Incl. GST) | Virtual CPE Meeting on WFH for CA Firms (Experience so far & Future Possibilities |

|

07-05-2021 Friday 08-05-2021 Saturday 14-05-2021 Friday 15-05-2021 Saturday |

3.00 p.m.

to

6.00 p.m. ₹ 1180/- (Incl. GST) |

Refresher Course on FEMA (Virtual) |

|

12-05-2021 Wednesday |

4.00 p.m.

to

6.30 p.m. ₹ 118/- (Incl. GST) |

WOW Series - Programme on Code of ethics and Income Tax (Virtual) |

|

13-05-2021 Thursday |

5.00 p.m.

to

7.00 p.m. ₹ 236/- (Incl. GST) |

Meeting on TDS Practical aspects and the way forward (Virtual) |

|

14-05-2021 Friday |

4.00 p.m.

to

7.00 p.m. ₹ 354/- (Incl. GST) |

Virtual CPE Meeting on Practice Development Strategies in current scenario & Networking of Firms |

|

15-05-2021

Saturday 16-05-2021 Sunday 21-05-2021 Friday 22-05-2021 Saturday & 23-05-2021 Sunday |

5.00 p.m.

to

7.00 p.m. ₹ 1180/- (Incl. GST) |

Refresher Course on Indirect Tax (Virtual) |

|

18/05/2021 Tuesday |

6.00 p.m. to 7.00 p.m. | Learning From Legend |

|

19-05-2021 Wednesday |

5.00 p.m.

to

7.00 p.m. ₹ 236/- (Incl. GST) |

Meeting on Plan your investments (Virtual) |

|

20-05-2021 Thursday |

5.00 p.m.

to

7.00 p.m. ₹ 236/- (Incl. GST) |

Virtual CPE Meeting on Audit in SAP Environment |

| 21-05-2021 to 29-05-2021 |

5.00 p.m.

to

8.00 p.m. ₹ 1180/- (Incl. GST) |

National Conference on Internal Audit (Virtual) |

|

22-05-2021 Saturday |

11.00 a.m.

to

1.00 p.m. ₹ 236/- (Incl. GST) |

Meeting on Unlocking Enterprise Value (Virtual) |

|

25-05-2021 Tuesday to 28-05-2021 Friday |

5.00 p.m.

to

8.00 p.m. ₹ 1180/- (Incl. GST) |

Refresher Course on NGOs & Charitable Organizations (Virtual) |

|

26-05-2021 Wednesday |

4.00 p.m.

to

6.00 p.m. ₹ 236/- (Incl. GST) |

Meeting on Wills and Succession Planning (Virtual) |

|

29-05-2021 Saturday |

4.00 p.m.

to

6.00 p.m. ₹ 236/- (Incl. GST) |

Meeting on Penalties under Income Tax Act (Virtual) |

|

Date & Day |

Time & |

Topic(s) |

Speaker(s) |

Regional Council Members |

Co-ordinators |

|---|---|---|---|---|---|

|

04-05-2021 09-05-2021 15 |

6.00 p.m. to 9.00 p.m. ₹ 2950/- (Incl. GST) |

Virtual Workshop on Excel Skill for Business |

CA. Priti Savla 9321426883 CA. Yashwant Kasar 9822488777 CA. Umesh Sharma 9822079900 |

CA. Akshay Taparia 7303448712 CA. Supriya Ausekar 7709676874 CA. Seema Baheti 9552598021 CA. Vivek Gupta 9867036565 |

|

|

Excel Skill for Business - Day to Day Operation in CA’s office |

CA. Nagarjunrao Akula |

||||

|

Data Validation • Excel functions & Formulas • Working with Multiple Worksheets & Workbooks • Advanced Formula Techniques • Data Cleaning and Preparation • Pivot Table • Graphs • Spreadsheet Chart • Pivot Chart • Lookup Table • Excel Macro • Excel Vba |

Prof. Ajay Pande |

||||

|

04-05-2021 02 |

5.00 p.m. to 7.00 p.m. ₹ 236/- (Incl. GST) |

Virtual CPE Meeting on WFH for CA Firms (Experience so far & Future Possibilities |

|

CA. Arpit Kabra CA. Balkishan Agarwal 9377110634 CA. Vimal Agrawal |

CA. Alok Jajodia 9821163916 CA. Abhishek Ruia 9833287183 CA. Abhinav Khurdia 7021868017 |

| Enabling WFH for your firm | CA. Mitesh Katira | ||||

| Panel Discussion: Experience of WFH so far & Future possibilities |

Moderator: CA. Dinesh Tejwani Panelists: |

||||

|

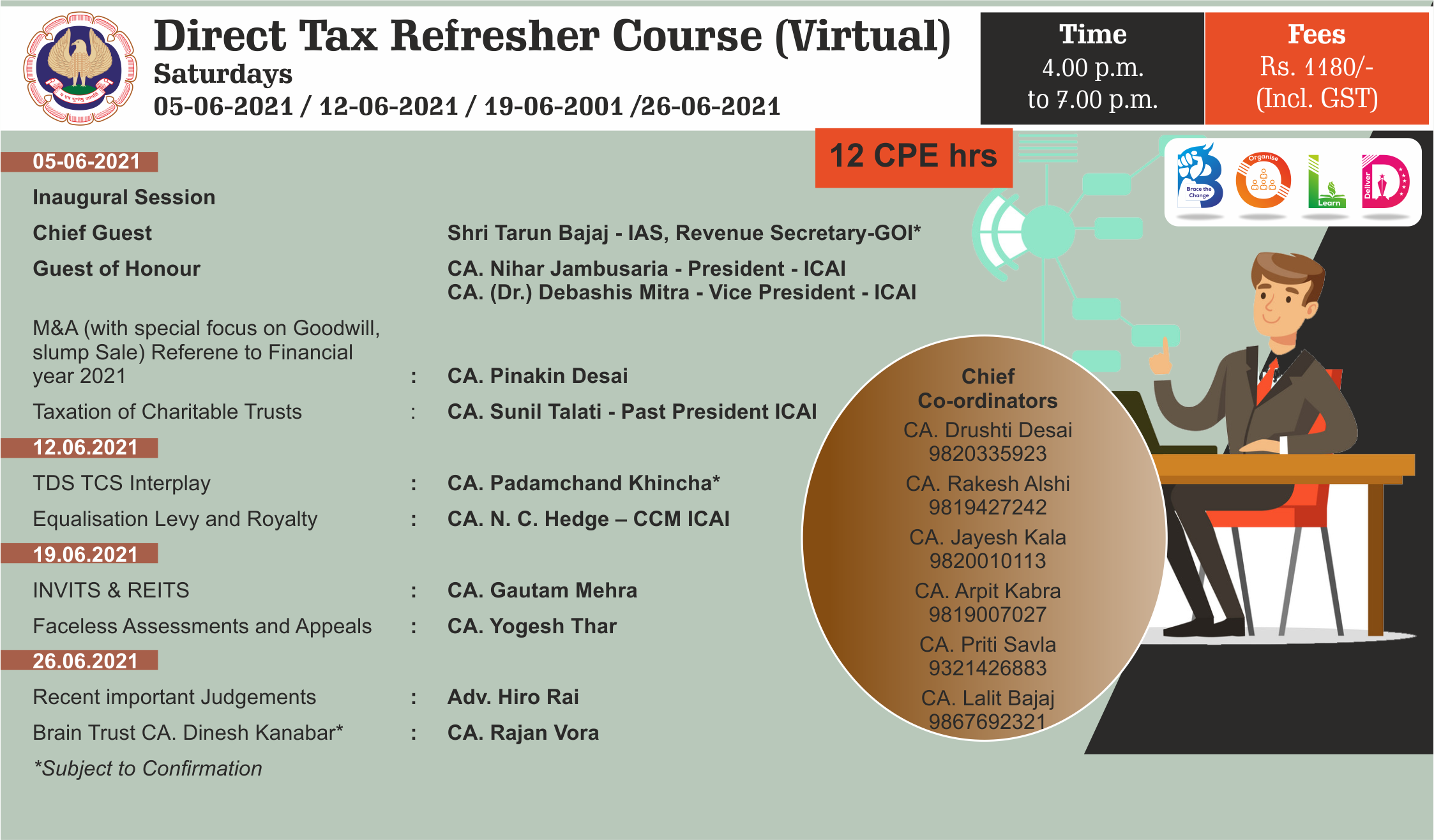

07-05-2021 08-05-2021 14-05-2021 15-05-2021 12 |

3.00 p.m. to 6.00 p.m. ₹ 1180/- (Incl. GST) |

Refresher Course on FEMA (Virtual) |

|

CA. Rakesh Alshi CA. Hitesh Pomal CA. Kamlesh Saboo CA. Vikash Jain |

CA. Bhavesh Shah 9821079625 CA. Nidhi Lalpuria 9322226910 CA. Santosh Jagdale 9819952502 |

| 07-05-2021 – 3.00 pm to 6.00 pm | |||||

| History and relevance, structure, sources of legislation, key definitions, Capital account vs. Current account transactions | CA. Manoj Shah | ||||

|

FDI & Foreign Investment - Sch 1, 4, 6 |

CA. Paresh P. Shah |

||||

| 08-05-2021 – 3.00 pm to 6.00 pm | |||||

| Bank accounts for non-residents and residents, LRS + $1 million scheme |

CA. Harshal Bhuta |

||||

|

Immovable property for NR and R |

CA. Natwar Thakrar |

||||

| 14-05-2021 – 3.00 pm to 6.00 pm | |||||

| LO/BO/PO |

CA. Hinesh Doshi |

||||

| ODI |

CA. Hardik Mehta |

||||

| 15-05-2021 – 3.00 pm to 6.00 pm | |||||

| ECB |

CA. Shabbir Motorwala |

||||

| FEMA Audit |

CA. Rajesh P. Shah |

||||

|

12-05-2021 02 |

4.00 p.m. to 6.30 p.m. ₹ 118/- (Incl. GST) |

WOW Series - Programme on Code of ethics and Income Tax (Virtual) |

|

CA. Drushti Desai CA. Priti Savla |

CA. Shweta Jain 9920737198 CA. Ruta Chitale 8390610136 CA. Pallavi Mayur 9850952424 |

| Code of Ethics | CA. Kemisha Soni, CCM, ICAI | ||||

| Income tax appellate law and procedure | CA. Krupa Gandhi | ||||

|

13-05-2021 02 |

5.00 p.m. to 7.00 p.m. ₹ 236/- (Incl. GST) |

Meeting on TDS Practical aspects and the way forward (Virtual) |

CA. Drushti Desai CA. Rakesh Alshi CA. Jayesh Kala |

CA. Ashita Shah 9769663120 CA. Monark Padmani 9978523838 CA. Nemish Shah 9429729679 |

|

|

TDS practical aspects and the way forward |

CA. Atul Suraiya |

||||

|

14-05-2021 03 |

4.00 p.m. to 7.00 p.m. ₹ 354/- (Incl. GST) |

Virtual CPE Meeting on Practice Development Strategies in current scenario & Networking of Firms |

|

CA. Priti Savla CA. Jayesh Kala CA. Yashwant Kasar |

CA. Alpesh Doshi 9892504512 CA. Premal Gandhi 9324383636 CA. Charvik Momaya 9004213066 |

| Practice Development Strategies in current scenario | CA Nilesh Vikamsey, Past President, ICAI | ||||

|

Panel Discussion on Networking of Firms |

CA Jay Chhaira, CCM - Moderator Panelists : |

||||

|

15-05-2021 16-05-2021 21-05-2021 22-05-2021 & 10 |

5.00 p.m. to 7.00 p.m. ₹ 1180/- (Incl. GST) |

Refresher Course on Indirect Tax (Virtual) |

CA. Umesh Sharma CA. Abhijit Kelkar CA. Lalit Bajaj |

CA. Sapna Loonawat 9325620758 CA. Renu Dawda 9403222888 CA. Harsh Bajaj 9821044319 CA. Gutam Lath 8655261203 |

|

| 15-05-2021 – 05.00 pm to 07.00 pm | |||||

| ITC and Issues ( U/s 16(2), 16(4), 17(5), Rule 36(4), etc) |

CA. Sunil Gabhawalla |

||||

| 16-05-2021 – 11.00 am to 01.00 pm | |||||

|

Important Judgements GST |

Adv. Rohit Jain |

||||

| 21-05-2021 – 05.00 pm to 07.00 pm | |||||

|

Attachment of Goods, Bank Account in GST? A legal debate |

Adv. Avinash Poddar |

||||

| 22-05-2021 – 05.00 pm to 07.00 pm | |||||

|

How to handle Departmental Audit and Notices under GST |

CA. A. R. Krishnan |

||||

| 23-05-2021 – 11.00 am to 01.00 pm | |||||

|

Fake Invoices, Frauds under GST and issues |

CA. Sushil Solanki, Ex Commissioner Service Tax

|

||||

|

18/05/2021 |

6.00 p.m. to 7.00 p.m. |

Learning From Legend |

CA. Bansi Mehta, Past President, ICAI |

CA. Drushti Desai 9820335923 CA. Arpit Kabra 9819007027 CA. Jayesh Kala 9820010113 |

|

|

19-05-2021 02 |

5.00 p.m. to 7.00 p.m. ₹ 236/- (Incl. GST) |

Meeting on Plan your investments (Virtual) |

CA. Drushti Desai CA. Hitesh Pomal CA. Lalit Bajaj |

CA. Forum Bhanushali 9930882903 CA. Deep Dedhia 9769654340 CA. Varsha Deshpande 9850453327 |

|

|

Plan your investments |

CA. Vipul Shah |

||||

|

20-05-2021 02 |

5.00 p.m. to 7.00 p.m. ₹ 236/- (Incl. GST) |

Virtual CPE Meeting on Audit in SAP Environment |

CA. Vishal P. Doshi CA. Balkishan Agarwal CA. Chintan Patel |

CA. Dinesh Tejwani 9987995349 CA. Aanchal Bagaria 9545631113 |

|

|

What SAPB1, SAP S/4 HANA, SAP ECC, SAP BYD can provide to the auditor |

Mr. Shashank Rameshwar |

||||

|

21-05-2021 to 29-05-2021 12 |

5.00 p.m. to 8.00 p.m. ₹ 1180/- (Incl. GST) |

National Conference on Internal Audit (Virtual) Friday 21.05.2021 Time: 05.00 pm to 08.00 pm |

|

CA. Murtuza Kachwala 9833015334 CA. Jayesh Kala 9820010113 CA. Vishal P. Doshi 9824059901 |

CA. Sanjay Nikam 9820446329 CA. Sumit Doshi 9377068248 |

|

Inaugural Address |

CA. C. S. Nanda, Chairman IASB - ICAI | ||||

|

Key Note Address - Increasing Opportunities in Internal Audit & Risk Advisory |

CA. Sunil Chandiramani, Independent Director, Magma Fin Corp, Ganesh Grains Pvt Ltd, UDS Ltd |

||||

|

For Internal Auditors: Rising Risks, Remote Teams and Real-time Testing |

CA. V. Swaminathan, Group Audit Head, Godrej Industries ltd |

||||

|

COVID-19 and IFC/IA: Practical Considerations While Navigating the Crisis |

Moderator: Mr. Sachin Shah, Director, Protiviti Panelists: CA. Avinash Sharma, Chief Audit Executive, Ooredoo, Myanmar Ltd CA. Joly Joseph, Director Internal Audit, Target Corporation CA. Deepak Saboo Rupnarayan, Vice President, HTA Pvt Ltd (Kantar) CA. Kiran Acharya, MD & CFO, Sandvik Asia Pvt Ltd. |

||||

|

Saturday 22.05.2021 Time: 05.00 pm to 08.00 pm |

|||||

|

Key Note Address - Information Technology Risks & Controls |

Eminent Faculty |

||||

|

Changing role of Internal Auditor - IT Audit Universe & Skills for IT Audit |

Mr. Vijai K. MD Technology Consulting, Protiviti |

||||

|

Evolving Technology & Changing Risk – Preparing for the New Normal |

Moderator: CA. Delzad D. Jivaasha, Associate VP - Risk Management - ICICI Lombard General Insurance Company Ltd. Panelists: CA. Navneet Khandelwal, CFO, Zensar Technologies CA. Jignesh Mehta, Regional Directior IA & Controls, Mondelez International, AMEA CA. Anil Phadtare, VP, Group head of Controls, Vodafone Group CA. Raviraj Karia, Sr. GM (IA), Intas Pharmaceuticals |

||||

|

Friday 28.05.2021 Time: 05.00 pm to 08.00 pm |

|||||

|

Key Note Address - Changing Technology |

Mr. Vilas Pujari - CIO - ACG Group |

||||

|

Driving Efficiency and Reliability with Continuous Control Monitoring |

Mr. Dhrubobrata Ghosh, MD, Protiviti |

||||

|

The Next Generation of Internal Auditing – Are You Ready? |

Moderator: CA Nikhil Thakkar, Head-IA, Honeywell India Panelists: CA. Rajiv Gupta, VP & Group Head, Flipkart CA. Sanjay Deodhar, Regional Audit Director, Cummins India CA. Vijayalakshmi, VP & Chief Internal Auditor, Voltas Ltd. CA. Jitendra Khatri, Associate Vice President, Valvoline |

||||

|

Saturday 29.05.2021 Time: 05.00 pm to 08.00 pm |

|||||

|

Key Note Address - Increasing Frauds and its nature |

Eminent Faculty |

||||

|

Fighting frauds with data driven insights |

CA. Shyam Periwal, Vice President & Global Head, UPL Ltd |

||||

|

Identifying Fraud during Internal Audit |

Moderator: Mr. Suprabhat NM, MD, Protiviti Panelists: CA. Surath Mukherjee, Executive Director, Dalmia Bharat Group CA. Pradip Rangani, Sector Head - Airport & Logistics, Adani Group Mr. Sanjay Mathur, VP & Head -Governance, Risk Mgmt & Compliance (GRC), Tata Communications Ltd CA. Girdhar K. Chitlangia, CFO, More Retail |

||||

|

22-05-2021 02 |

11.00 a.m. to 1.00 p.m. ₹ 236/- (Incl. GST) |

Meeting on Unlocking Enterprise Value (Virtual)

|

CA. Drushti Desai CA. Sushrut Chitale CA. Murtuza Kachwala |

CA Renuka Boramnikar

8805153100 CA Bhavin Mehta 9974741312 |

|

| Unlocking Enterprise Value |

CA Asit Mehta |

||||

|

25-05-2021 to 28-05-2021 12 |

5.00 p.m. to 8.00 p.m. ₹ 1180/- (Incl. GST) |

Refresher Course on NGOs & Charitable Organizations (Virtual) |

CA. Murtuza Kachwala CA. Hitesh Pomal CA. Kamlesh Saboo |

CA. Vipul Shah 9820604323 CA. Hardik Dave 9820818018 CA. Jitesh Kedia 9930178329 |

|

|

25-05-2021 – 5.00 pm to 8.00 pm |

|||||

| Formation and Registration of Trusts, Societies under MPT Act |

CA. Suhas Malankar |

||||

|

Important compliances under Maharashtra Public Trusts Act |

CA. Vipin Batavia |

||||

| 26-05-2021 – 5.00 pm to 8.00 pm | |||||

|

Taxation of NGO’s Excluding Fresh/New registration procedure |

CA. Sanjiv Brahme |

||||

|

Fresh /New registration procedure under Income Tax |

CA. Rajesh Kadakia |

||||

|

27-05-2021 – 5.00 pm to 8.00 pm |

|||||

| Applicability of GST to NGOs |

CA. Ronak Thakkar |

||||

|

Accounting & Auditing under different laws applicable to NPO |

CA. (Dr.) Kishore Peshori |

||||

|

28-05-2021 – 5.00 pm to 8.00 pm |

|||||

| FCRA provisions applicable to NGOs including recent amendment |

CA. (Dr.) Gautam Shah |

||||

|

CSR provisions and their compliance by companies |

CA. Aniket Talati* - CCM-ICAI |

||||

|

26-05-2021 02 |

4.00 p.m. to 6.00 p.m. ₹ 236/- (Incl. GST) |

Meeting on Wills and Succession Planning (Virtual)

|

CA. Drushti Desai CA. Arpit Kabra CA. Anand Jakhotiya |

CA. Charmi Shah 9833917620 CA. Milind Rach 9987360505 CA. Smita Bafna 9422209501 |

|

| Wills and Succession Planning |

CA Anup Shah |

||||

|

29-05-2021 02 |

4.00 p.m. to 6.00 p.m. ₹ 236/- (Incl. GST) |

Meeting on Penalties under Income Tax Act (Virtual) |

CA. Drushti Desai CA. Priti Savla CA. Vimal Agrawal |

CA. Ryan Fernandes 7718897836 CA Rekha Patwardhan 937391883 |

|

| Penalties under Income Tax Act |

CA Jagdish Punjabi |

* subject to confirmation

Law Updates

| Direct Tax | CA. Haresh Kenia, CA. Deepak Lala, CA. Gopal Bohra |

| Direct Tax – Recent Judgment | CA. Paras Savla, CA. Ketan Vajani |

| International Taxation | CA. Hinesh Doshi, CA. Pramita Rathi |

| CENTRAL GST | CA. Rajiv Luthia, CA. Jinit Shah |

| Corporate Laws | CA. Premal Gandhi, CS. Mahesh Soni |

| Transfer Pricing | CA. Bhavya Bansal, CA. Bhavesh Dedhia, CA. Shazia Khatri |

| STATE GST | CA. C. B. Thakar, CA. Madhav Kalani |

| Co-operative Housing Societies | CA. Ramesh Prabhu, CA. Sunil Nagonkar |

| MAHARERA | CA. Ashwin Shah, CA. Mahadev Birla |

| Insolvency and Bankruptcy Code | CA. Pravin Navandar, CA. Mukund Mall |

| HOW INTERNAL AUDIT CAN HELP TO IMPROVE EBIDTA | CA Shashank Sah, CA. Huzeifa Unwala |

| SEBI | CA. BhaveshVora, CA Jayant Thakur |

| RBI / NBFC Circular | CA Abhijit Sanzgiri, CA. Sanjay Khemani |

| Merger and Acquistion | CA. Sujal Shah, CA. Ushma Shah |

CA. Haresh Kenia, CA. Deepak Lala, CA. Gopal Bohra

Applicability of reporting under Clause 30C & 44 of Tax Audit report deferred

CIRCULAR NO. 5/2021 DATED 25TH MARCH, 2021

The Central Board of Direct Taxes, vide Circular dated 25th March, 2021, has deferred the applicability of reporting under clause 30C & 44 of Form 3CD till 31st March, 2022. The Board had initially deferred the applicability of this clause three times. Considering the prevailing situation due to Covid-19 pandemic across the country, the applicability has been further deferred.

- Clause 30C requires disclosures in respect of impermissible avoidance agreement

- Clause 44 requires break-up of total expenditure of entities registered or not registered under GST

Notification of rules for re-registration/ re-approval of charitable trust

NOTIFICATION G.S.R. 212(E) [NO. 19/2021/ F. No. 370142/4/2021-TPL] DATED 26TH MARCH, 2021

The Central Board of Direct Taxes, vide Notification G.S.R. 212(E) dated 26th March, 2021, has notified rules for re-registration/ re-approval of charitable trusts, setting forth the detailed procedures to be followed, forms to be filled, and documents to be attached. The rules inserted/modified are:

- Modified Rule 2C, for re-approval u/s 10(23C)

- Inserted Rule 5CA, for re-approval u/s 35(1)

- Modified Rule 11AA, for re-approval u/s 80G(5)(vi)

- Modified Rule 17A, for re-registration u/s 12A

DTAA between GOVERNMENT OF REPUBLIC OF INDIA and GOVERNMENT OF ISLAMIC REPUBLIC OF IRAN- Section 90 of Income Tax Act.

The Central Government , in exercise of the powers conferred by sub-section (1) of section 90 of the Income-tax Act, vide NOTIFICATION S.O. NO. 1442(E) [NO.29/2021/F.NO.501/03/92-FTD-II], dated 1-4-2021 hereby notifies agreement between THE GOVERNMENT OF THE REPUBLIC OF INDIA AND THE GOVERNMENT OF THE ISLAMIC REPUBLIC OF IRAN for the avoidance of double Taxation and the prevention of fiscal evasion with respect to taxes on income .

- Relaxation of certain provisions of Specified Act – Extension of due date for Completion of action under Specified Acts- - Read with sections 139AA, 144C, 148, 149 and 151 Income tax Act and Section 168 of the Finance Act ,2016

The Central Government vide NOTIFICATION S.O. 1432(E) [NO. 20/2021/F. NO. 370142/35/2020-TPL], DATED 31-3-2021 and in exercise of the powers conferred by section 3 (1) of the Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020 and subsequent notifications issued under this Act, hereby extends the following due dates in view of the COVID-19 pandemic, certain time limits specified under the various tax and Benami laws

- The extended last date for intimating Aadhaar number for the purposes of linking Aadhaar with PAN is 31st March, 2021. Keeping in view the difficulties faced by the taxpayers, the Central Government has issued notification today extending the last date for the intimation of Aadhaar number and linking thereof with PAN to 30th June, 2021.

- The said notification also extended time-limits for issue of notice under section 148 of the Act, passing of consequential order under section 144C for direction issued by the Dispute Resolution Panel (DRP) and processing of equalisation levy statements to 30th April, 2021.

- Tax Audit Report in form 3CD amended

The Central Board of Direct Taxes exercise of the powers conferred by section 44AB read with section 295 of the Income-tax Act vide NOTIFICATION NO. G.S.R. 246(E) [NO. 28/2021/F. NO 370142/9/2018-TPL], DATED 1-4-2021 gives the Income-tax (eighth Amendment) Rules, 2021

It has amended the Tax Audit Report (TAR) in Form 3CD in order to incorporate the changes brought in the Income Tax Act by the Finance Act, 2021. These changes in Form 3CD shall be effective from the 1st day of April 2021 and shall apply for the assessment year 2021-22 are as under .

Revised Tax Audit Report in certain cases

Rule 6G prescribes rules related to reporting of the audit of accounts to be furnished under section 44AB. For allowing filing of revised Tax Audit Report, Rule 6G is amended to insert a sub-rule (3) as mentioned below-

“The report of audit furnished under this rule may be revised by the person by getting revised report of audit from an accountant , duly signed and verified by such accountant, and furnish it before the end of the relevant assessment year for which the report pertains, if there is payment by such person after furnishing of report under subrule (1) and (2) which necessitates recalculation of disallowance under section 40 or section 43B.”

Changes in Clause 8A to report exercise of option under section 115BAC/115BAD

The Finance Act 2020 has introduced two new concessional tax rate regime under section 115BAC for Individuals and HUF and section 115BAD for cooperative societies. The two provisions are applicable from AY 2021-22. Ans in order to incorporate the same in the Tax Audit Report, Clause 8a of Form 3CD is changed to include these two sections - section 115BAC and section 115BAD also.

Adjustment in WDV of Assets For exercising option under sections 115BAC/115BAD

There was amendment in Form 3CD for the AY 2020-21 where in Clause 18(ca) was introduced to report the adjustment in WDV of the block of assets if lower tax regime under section 115BAA is exercised by the assessee. This clause was valid for AY 2021-22 only.

The finance Act 2020, introduced two new concessional tax rate regimes under section 115BAC for Individuals and HUF and section 115BAD for cooperative societies. The two provisions are applicable from AY 2021-22. In cases of section 115BAC and section 115BAD also, additional depreciation is not allowed and hence requires adjustment in WDV of the block of assets. Hence Clause 18(ca) is substituted with the new sub-clause (ca) which is applicable for AY 2021-22 only.

Higher safe harbour rule of 20% between actual sales consideration and stamp duty value under section 43CA and section 56(2)(x) - Amendment in Clause 17 of form 3CD

In order to boost demand in the real-estate sector and to enable the real-estate developers to liquidate their unsold inventory at a rate lower than the Stamp duty rate and giving benefit to the home buyers, the finance Act 2021, has amended the provision of section 43CA and Section 56(2)(x) of the Act and it provides for increase the safe harbour from 10% to 20% under section 43CA for the period from 12th November 2020 to 30th June 2021 in respect of the only primary sale of residential units of value up to Rs. 2 crore.

Consequential relief by increasing the safe harbour from 10% to 20% was also allowed to buyers of these residential units under section 56(2)(x) for the said period. Therefore, for these transactions, the Stamp duty rate shall be deemed as a sale/purchase consideration only if the variation between the agreement value and the stamp duty rate is more than 20%.

These changes are now incorporated in Form 3CD from AY 2021-22. For this purpose, existing clause 17 is substituted with the new Clause 17 incorporating the above amendment.

Depreciation of Goodwill - Changes in Clause 18 of Form 3CD

Finance Act, 2021 brought an amendment by which depreciation under section 32 on goodwill is denied. It is further provided that the block containing the goodwill as an asset shall be modified and depreciation on goodwill as appearing in that block at the WDV as of 1.4.2020 shall not be claimed from AY 2021-22 and such value of goodwill will be excluded from the block. The block needs to be modified to that extent. Accordingly, Form 3CD has made the necessary changes in clause 18. A new sub-clause (cb) is inserted in Clause 18 of Form 3CD for reporting the adjustment in WDV of the block of assets -

Adjustment in brought forward of losses if option u/s 115BAC/115BAD is exercised - Changes in Clause 32 of form 3CD

The new tax regime under section 115BAA, section 115BAC and section 115BAD do not allow certain deductions and if the option under these provisions is exercised then the brought forward losses need to be modified to the extent they are related to such restricted disallowed deductions. Similar to changes in clause 8a and clause 18, Clause 32 of the Form 3CD is also amended to include section 115BAC and section 115BAD in the reporting requirement

Clause 36 related to DDT Omitted

Finance Act 2020 has abolished the Dividend Distribution Tax (DDT) and reverted the classic system of taxation of dividend income in the hands of the shareholders/recipients. Hence companies are not required to pay any dividend distribution tax from FY 2020-21. Accordingly, Clause 36 of the existing Form 3CD is omitted from reporting requirement from AY 2021-22.

New Income Tax Return Forms for AY 2021-22

The Central Board of Direct Taxes In exercise of the powers conferred by section 139, read with section 295 of the Income-tax Act, vide NOTIFICATION G.S.R. 242(E) [NO. 21/2021/F.NO. 370142/5/2021-TPL], DATED 31-3-2021, gives the Income-tax (7th Amendment) Rules, 2021. It shall come into force from 01.04.2021. It notifies the Income Tax Return Forms (ITR Forms) ITR-1 to ITR-7 for the Assessment Year 2021-22.

The CBDT vide Press note dated 01.04.2021 indicated that , keeping in view the ongoing crisis due to COVID pandemic and to facilitate the taxpayers, no significant change have been made to the ITR Forms in comparison to the last year’s ITR Forms. Only the bare minimum changes necessitated due to amendments in the Income-tax Act, 1961 have been made. Accordingly, the notified ITR forms do not contain any major amendments or changes compared to the preceding year except a few to incorporate the changes or amendments in the Finance Act of the relevant year.

CBDT has amended Rule 12 of the Income Tax Rules,1962 to incorporate the changes related to ITR forms for the AY 2021-22. There is no change in the manner of filing ITR Forms as compared to last year. The following changes are notified for the ITR forms ITR-1 to ITR-7 for the AY 2021-22

In Rule 12(1), the year ‘2021’ is replaced for the figure ‘2020’ to make the changes applicable for AY 2021-22.

ITR-1 cannot be used for return filing if the tax has been deducted under Section 194N. Thus, a person is ineligible to file his return of income in ITR-1 for AY 2021-22 if tax is deducted under section 194N.

ITR-1 cannot be used for return filing if the tax has been deferred in respect of ESOPs allotted by an eligible start-up under section 191 ( 2) or section 192 (1C) of the Act.

ITR-4 cannot be used for return filing if the tax has been deferred in respect of ESOPs allotted by an eligible start-up under section 191 ( 2) or section 192 (1C) of the Act

Deferment of reporting requirement under Clause 30C and Clause 44 of Tx Audit report in Form -3 CD – Section 119, read with section 44AB of Income tax Act.

CBDT vide CIRCULAR NO. 5/2020 [F. NO. 370142/9/2018-TPL], DATED 25-3-2021 issued following instruction to Subordinate authorities

Section 44AB of the Income-tax Act, 1961 read with rule 6G of the Income-tax Rules, 1962 requires specified persons to furnish the Tax Audit Report along with the prescribed particulars in Form No. 3CD. The existing Form No. 3CD was amended vide Notification No. GSR 666(E) dated 20th July, 2018 with effect from 20th August, 2018. However, the reporting under clause 30C and clause 44 of the Tax Audit Report was kept in abeyance till 31st March, 2019 vide Circular No. 6/2018 dated 17-8-2018, which was subsequently extended to 31st March, 2020 vide Circular No. 9/2019.Vide circular no. 10/2020, dated 24-4-2020, it was further extended to 31st March, 2021.

In view of the prevailing situation due to COVID-19 pandemic across the country, it has been decided by the Board that the reporting under clause 30C and clause 44 of the Tax Audit Report shall be kept in abeyance till 31st March, 2022

Clarification on provision of Direct Tax VIVAD SE VISHWAS Act, 2020 - Faq No. 70 of Circular No. 21/2020 modified relating to Search cases.

CIRCULAR NO. 4/2021 [F. NO. IT (A)/1/2020-TPL], DATED 23-3-2021

Sections 10 and 11 of Vivad se Vishwas empower the Central Government/Central Board of Direct Taxes to issue directions or orders in public interest or to remove difficulties. In order to facilitate the taxpayers, clarifications under the said sections in form of answers to frequently asked questions (FAQs) were issued vide Circular No. 9/2020 dated 22nd April, 2020 (covering FAQ 1-55) and Circular No. 21/2020 dated 4th December, 2020 (covering FAQ Nos. 56-89).

FAQ No. 70 of Circular No. 21/2020 clarified eligibility for search case under Vivad se Vishwas. It was clarified that if the assessment order has been framed in the case of a taxpayer under section 143(3)/144 of the Income-tax Act based on the search executed in some other taxpayer’s case, it is to be considered as a ‘search case’ under Vivad se Vishwas

Several representations have been received seeking further clarity with regard to the classification of a case as a ‘search case’ for the purposes of Vivad se Vishwas. The matter has been examined. In order to remove any uncertainty in this regard, and in exercise of powers under sections 10 and 11 of Vivad se Vishwas, it is hereby clarified that a ‘search case’ means an assessment or reassessment made under sections 143(3)/144/147/153A/153C/158BC of the Income-tax Act in the case of a person referred to in section 153A or section 153C or section 158BC or section 158BD of the Income-tax Act on the basis of search initiated under section 132, or requisition made under section 132A of the Income-tax Act. The FAQ No. 70 of Circular No. 21/2020 stands modified to this extent.

Amendment of Rule 10DA, Rule 10DB and Form No. 3CEAB relating to maintenance and furnishing of information and documents by constituent entity and furnishing of Report in respect of an international group

The Central Board of Direct Taxes, in exercise of the powers conferred by sub-section (1) and sub-section (4) of section 92D and sub-section (8) of section 286, read with section 295 of the Income-tax Act, vide NOTIFICATION G.S.R 250(E) [ NO. 31/2021/F.NO.370142/19/2019-TPL], DATED 5-4-2021, gives the Income-tax (9th Amendment) Rules, 2021. It shall come into force on the 1st day of April, 2021 relevant to the Assessment Year 2021-22. It amends rule 10 DA , 10 DB and form 3CEAB.

Rule 10 DA prescribes the maintenance and furnishing of information and documents by constituent entity of an international group under section 92D in respect of an international group.

Presently , rule 10DA(2) requires furnishing of the information in Form 3CEAA to the Joint Commissioner on or before the due date for furnishing the return of income as specified under sub-section (1) of section 139. The 9th Amendment Rules has substituted the word ‘Commissioner’ to ‘Director’. Hence, now it requires furnishing of the information in Form 3CEAA to the Joint Director on or before the due date for furnishing the return of income as specified under sub-section (1) of section 139.

Presently, rule 10DA(4) provides that where there are more than one constituent entities resident in India of an international group required to file the information and document under Rule 10DA(2), the Form 3CEAA may be furnished by any one constituent entity under the following circumstances-

(i) the international group has designated such entity for this purpose; and

(ii) the information has been conveyed in Form No. 3CEAB to the Joint Commissioner on this behalf thirty days before the due date of furnishing Form No. 3CEAA

The 9th Amendment Rules, 2021 substituted the ‘constituent entities resident in India of an international group’ with ‘constituent entities’. Hence, now it henceforth covers all the constituent entities whether are resident in India or not of the international group. Now, Form 3CEAA is required to be filed by any one of the entities designated in Form 3CEAB for both resident and non-resident entities. The Corresponding amendment is notified in Form 3CEAB to modify the heading of the form to omit the words ‘resident in India’. Further, similar to sub-rule(1), the amendment in sub-rule (4) provides for the furnishing of information to the Joint Director in place of the Joint Commissioner

It also amends rule 10DB which deals with the furnishing of Report in respect of an International Group under section 286 of the Act and it presently prescribes that the income-tax authority for the purposes of section 286 shall be the Joint Commissioner as may be designated by the Director-General of Income-tax (Risk Assessment). This is now substituted with a new sub-rule from 1-4-2021. The 9th Amendment Rules now substitutes the Joint Commissioner with the Joint Director and Director General of Income-tax (Risk Assessment) with Principal Director General of Income-tax (Systems) or the Director-General of Income-tax (Systems).

Presently rule 10DB (6) provides that for the purpose of Section 286(7) an international group shall furnish the report if the total consolidated group revenue, as reflected in the consolidated financial statement for the accounting year preceding such accounting year does not exceed Rs 5500 crore. The 9th Amendment Rules now increased the limit to Rs. 6400 crore. Thus, for CbCR (Country-by-Country Reporting) related compliances to be applicable, the International group’s consolidated group revenue shall have to exceed Rs. 6400 crore applicable from 1-4-2021.

Determination of Income for TDS on Payment to Non-residents u/s 195 – Insertion of Rule 29BA and Form 15E

The Central Board of Direct Taxes , in exercise of the powers conferred by section 195, read with section 295 of the Income-tax Act, vide NOTIFICATION NO. G.S.R. 194(E) [NO. 18/2021 F. NO. 370142/24/2019-TPL], DATED 16-3-2021, gives the Income-tax (5th Amendment) Rules, 2021. It shall come into force with effect from the 1st day of April, 2021.

It inserts new Rule 29BA and Form 15E in the Income Tax Rules, 1962 for determining the sum chargeable to tax for the purpose of TDS on payments to non-residents as per section 195(2) of the Income Tax Act. This is the facility provided by the Income Tax department for online filing of applications seeking a determination of tax to be deducted at source on payment to non-residents.

Presently before this amendment ,under section 195(2) of the Act, if a person who is responsible for paying any sum to a non-resident which is chargeable to tax under the Act considers that the whole of such sum would not be income chargeable to tax in the case of the recipient, he can make an application to the Assessing Officer to determine the appropriate proportion of such sum chargeable. This provision is used by a person making payment to a non-resident to obtain a certificate/order from the Assessing Officer for lower or nil withholding tax. This process is manual. In order to use technology to streamline the process, which will not only reduce the time for processing of such applications but shall also help tax administration in monitoring such payments, Finance (No. 2) Act, 2019 has amended the provisions of section 195(2) to provide for filing of online applications for a lower or nil TDS certificate under section 195. After the amendment, a non-resident can apply online in electronic form for a lower or nil TDS certificate under section 195 from the sum payable to a non-resident. This was subject to the rules to be prescribed by the CBDT in this regard. It amended the provisions of section 195 (2) to allow for prescribing the form and manner of application to the Assessing Officer and also for the manner of determination of the appropriate portion of sum chargeable to tax by the Assessing Officer. Once such sum or income is determined after the application is filed online in the prescribed form, tax shall be deducted under section 195(1) only on that proportion of the sum which is chargeable to tax. A similar amendment was also made in section 195(7) which is applicable to a specified class of persons or cases.

- The application is required to be made in Form 15E electronically.

- Form 15E shall be verified by digital signature or through electronic verification code (EVC).

- The Assessing Officer after examining the application so made in Form 15E, shall determine the sum that is chargeable to tax in India.

- The Assessing Officer shall be required to issue a certificate mentioning the appropriate proportion of such sum chargeable to tax.

- The Assessing Officer shall take into consideration the followings while examining the

application-

- tax payable on estimated income for the previous year in which application is filed

- tax payable on preceding four previous year’s income

- outstanding demand under the Income Tax Act/Wealth Tax Act

- advance tax, TDS/TCS for the previous year in which application is filed

- The certificate shall be valid only for the payment to non-resident named therein and for such period of the previous year as may be specified in the certificate, unless it is cancelled by the Assessing Officer at any time before the expiry of the specified period.

- The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) shall prescribe the procedures, formats and standards for online filing of the application in Form 15E.

- Registration Procedure u/s 12AB for Trust and Others- Jurisdiction for Online Registration and Cancellation

The Central Board of Direct Taxes vide NOTIFICATION NO. G.S.R. 212 (E) [NO. 19/2021/F. NO. 370142/4/2021-TPL], DATED 26-3-2021, gives the Income-tax (6th Amendment) Rules, 2021. It shall come into force on the 1st day of April, 2021. It notifies the new registration procedure for Charitable Trusts and other institutions under section 12AB and section 10(23C) through Income-tax (6th Amendment) Rules, 2021. It further notifies the procedure for furnishing the statement of donation received by NGOs/Trusts under section 80G(5).

The new registration scheme for Charitable Trusts and others was first introduced in the statute by the Finance Act, 2020 and was made effective from 1st June 2020. However, due to the COVID-19 pandemic outbreak and consequent nation-wide lockdown, the registration procedure under new section 12AB was postponed and deferred to 1st October 2020. This was further deferred to 1st April 2021. Both the renewal of registration u/s 12A or section 12AA, as well as renewal of approval under section 80G, was deferred. Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020 rationalized the procedure relating to approval/ registration/ notification of certain entities referred to in sections 10(23C), 12AA, 35 and 80G of the Act effective from 1st April 2021.

Under the new registration regime under section 12AB,it is provided that the registration will remain valid for a period of 5 years and shall be required to be renewed after every 5 years, unlike the present system of perpetual registration once granted.

It amends Rule 5C and 5F

It Substitutes Rule 2C, 11AA, 17A and Form no. 10A;

It Substitutes Form No. 3CF for Form Nos 3CF-I, 3CF-II AND 3CF-III;

It Inserts Rules 5CA & 18AB and Form Nos. 10AB, 10AC, 10AD, 10BD, and 10BE;

It Omits Form no. 56

The notification no 19 / 2021 has also introduced various forms for approval and registration as detailed below. These forms for application for registration or approval are required to be furnished to the Principal Commissioner or Commissioner authorised by the Board in this behalf.

Form Name Related Rules Purpose

Form 10A Rules 2C or 5CA or 11AA or 17A Application for registration or provisional registration or intimation or approval or provisional approval

Form 3CF Rules 5C, 5D, 5E and 5F Application for registration or approval

Form 10AB Rules 2C or 11AA or 17A Application for registration or approval

Form 10AC Rules 2C or 11AA or 17A Order for registration or provisional registration or approval or provisional approval

Form 10AD Rules 2C or 11AA or 17A Order for registration or approval or rejection or cancellation

Form 10BD Rule 18AB Statement of particulars to be filed by reporting person under section 80G(5)(viii) and section 35(1A)(i)

Form 10BE Rule 18AB Certificate of donation under section 80G(5)(ix) and under section 35(1A)(ii)

Amendment in Rule 5C

Rule 5C is amended which deals with filing of an application for the purpose of grant of approval for the exemption u/s 35(1)(ii)/(iii) for scientific research association or university etc. The amended Rule 5C has substituted Form No. 3CF-I and Form No. 3CF-II with a new Form 3CF for application for approval u/s 35(1)(ii)/(iii). Now Form No 3CF is required to be furnished online electronically and shall be verified by the person who is authorised to verify the return of income under section 140 of the Act with digital signature (DSC) or EVC. If the return of income of the applicant is required to be furnished under digital signature, then furnishing Form 3CF with DSC is compulsory else the forms can be furnished with EVC.

New Rule 5CA inserted

It inserts new rule 5CA for filing of application for intimation under 5th proviso to section 35(1). The application for intimation under the 5th proviso shall be made in Form 10A.The Certain documents are required to be submitted along with Form No. 10A. Readers are requested to refer to detailed notification for specified documents to be submitted. Form Nos. 10A is required to be furnished online electronically and shall be verified in the similar manner as provided under Rule 5C above. On receipt of an application in Form No. 10A, the Principal Commissioner or Commissioner shall issue a sixteen-digit alphanumeric Unique Registration Number (URN) to the applicants. If, at any point of time, it is noticed that Form No. 10A has not been duly filled in by not providing, fully or partly, or by providing false or incorrect information or documents or by not complying with the requirements of Rule 5CA(3) or (4), then the Principal Commissioner or Commissioner after giving an opportunity of being heard, may cancel the Unique Registration Number (URN) so issued and such Unique Registration Number (URN) shall be deemed to have never been issued.

Amendment in Rule 5F

Rule 5C is amended which deals with filing of an application for the purpose of grant of approval for the exemption u/s 35(1)(iia) for a scientific research company. The amended Rule 5C has substituted Form No. 3CF-III with a new Form 3CF for application for approval u/s 35(1)(iia). Form No 3CF is required to be furnished online electronically. Form 3CF shall be verified by the person who is authorised to verify the return of income under section 140 of the Act with digital signature (DSC) or EVC. If the return of income of the applicant is required to be furnished under digital signature, then furnishing Form 3CF with DSC is compulsory else the forms can be furnished with EVC.

Substitution of Rule 11AA

Rule 11AA is substituted with new rule. Rule 11AA deals with requirements for approval of an institution or fund under section 80G (5)(vi).An application under clause (i) or clause (iv) of the first proviso to section 80G(5) for the grant of approval of a fund or institution shall be made in Form 10A. Where application is made under clause (i) or clause (iv) of the first proviso to section 80G(5), the application shall be made in Form 10AB.The Certain documents are required to be submitted along with Form Nos. 10A or 10AB. Readers are requested to refer to detailed notification for specified documents to be submitted. Form Nos. 10A/10AB is required to be furnished online electronically and shall be verified in the same manner as rule 5C above. The procedure as regard issue and cancellation of Unique Registration Number (URN) are also similar to as provided under rule 5CA above.

Where an application for approval is made by a new institution or fund under clause (iv) of first proviso to section 80G(5), the provisional approval shall be effective from the date of order in Form 10AC.Where an application is made in Form 10AB, the order of approval or rejection or cancellation shall be in Form 10AD and in case approval is granted, sixteen digit alphanumeric number Unique Registration Number (URN) shall be issued, by the Principal Commissioner or Commissioner.

Substitution of Rule 17A

Rule 17A is substituted with new rules. Rule 17A deals with application for registration of charitable or religious trusts, NGOs, etc. under sub- clause (i) or sub-clause(ii) or sub-clause(iii) or sub-clause(iv) or sub-clause(v) or sub-clause(vi) of clause (ac)of sub-section (1) of section 12A. An application under clause (i) or clause (vi) of section 12A(1)(ac) for the grant of approval of a fund or institution shall be made in Form 10A. Where application is made under clause (ii)/(iii)(iv) or clause (v) of section 12A(1)(ac), the application shall be made in Form 10AB. The certain documents are required to be submitted along with Form Nos. 10A or 10AB. Readers are requested to refer to detailed notification for specified documents to be submitted. electronically and shall be verified in the same manner as rule 5C above. The procedure as regard issue and cancellation of Unique Registration Number (URN) are also similar to as provided under rule 5CA above.

Where an application for approval is made by a new Trust under section 12A(1)(ac)(vi) during previous year beginning on 1st day of April, 2021, the provisional registration shall be effective from the assessment year beginning on 1st day of April, 2022.Where an application is made in Form 10AB, the order of registration or rejection or cancellation shall be in Form 10AD and in case registration is granted, sixteen digit alphanumeric number Unique Registration Number (URN) shall be issued, by the Principal Commissioner or Commissioner.

Insertion of New Rule 18AB

Rule 18AB is inserted in relation to Furnishing of Statement of particulars and certificate under section 80G(5)(viii)/(ix) or under section35(1A). it requires furnishing of statement of donation received and issue of donation certificates to the donors for claiming deduction from the gross total income. This notification has framed the rules for furnishing such statements and certificates of donation to donors. Such statements are required to be filed electronically from the financial year 2021-22. Statement of particulars required to be furnished by any research association, university, college or other institution or company or fund (“reporting person”) under clause (viii) of sub-section (5) of section 80G or under clause (i) to sub-section (1A) of section 35 shall be furnished in respect of each financial year, beginning with the financial year 2021-2022, in Form No. 10BD and shall be verified in the manner indicated therein. The reporting person shall report the aggregate amount of donation received from each person in the financial year for which the statement is furnished. Where donation is received from more than one person, the proportionate amount of each person shall be reported. Where no proportion is specified by the donors, the same shall be proportioned equally. The statement of donation in Form 10BD is required to be furnished online electronically. Form No. 10BD shall be verified by the person who is authorised to verify the return of income under section 140 of the Act with digital signature (DSC) or EVC.

If the return of income of the applicant is required to be furnished under digital signature, then furnishing Form 10BD with DSC is compulsory else the forms can be furnished with EVC. The reporting person is required to furnish a certificate of donation (as referred to in clause (ix) of sub-section (5) of section 80G or in clause (ii) to sub-section (1A) to section 35), to the donor in Form No. 10 BE specifying the amount of donation received during financial year from such donor, beginning with the financial year 2021-2022.The certificate of donation in Form 10BE is required to be generated and downloaded from the income tax portal to be implemented by the Pr. DGIT/DGIT (Systems).The certificate of donation is required to be furnished to the donor on or before the 31st May, immediately following the financial year in which the donation is received. The statement of donations received in a financial year shall be required to be furnished by 31st May, immediately following the financial year in which the donation is received.

Readers are requested to read the detailed notification referred here in above.

CA. Paras Savla, CA. Ketan Vajani

Rejection of registration u/s. 12AA in the case of a trust running educational trust for the reason of acceptance of capitation fees held justified

Assessee was a charitable trust and was running an educational institution. A search operation was carried out in the office of the assessee and various documents were seized. The seized documents revealed receipt of capitation fees by the assessee. The Treasurer and secretary of the trust in their statements had also admitted that trust was collecting capitation fee for admission of students. For this reason, the Commissioner rejected application of assessee for grant of registration under section 12AA. The same was upheld by the Tribunal on the ground that trust was not running charitable activities. The decision of the Tribunal was affirmed by the High Court. On appeal by the assessee, the Supreme Court held that there was no ground to interfere with impugned order of High Court and instant appeal filed against same was to be dismissed. The Supreme Court accordingly affirmed the order of the High Court reported at Travancore Education Society v. CIT [2016] 66 taxmann.com 362/[2014] 369 ITR 534 (Ker.)

Karnataka Chamber of Commerce and Industry Vs. CIT Hubli (2021) 126 taxmann.com 21 (SC)

Automatic vacation of stay granted by Tribunal upon expiry of 365 days held arbitrary and discriminatory and therefore liable to be struck down as offending Article 14 of the Constitution

Since the object of the third proviso to Section 254(2A) is the automatic vacation of a stay that has been granted on the completion of 365 days, whether or not the assessee is responsible for the delay caused in hearing the appeal, such object being itself discriminatory is liable to be struck down as violating Article 14 of the Constitution of India. Also, the said proviso would result in the automatic vacation of a stay upon the expiry of 365 days even if the Appellate Tribunal could not take up the appeal in time for no fault of the assessee. Further, vacation of stay in favour of the revenue would ensue even if the revenue is itself responsible for the delay in hearing the appeal. In this sense, the said proviso is also manifestly arbitrary being a provision which is capricious, irrational and disproportionate so far as the assessee is concerned.

Consequently, the third proviso to Section 254(2A) will now be read so as to ensure that the stay of demand shall stand vacated after the expiry of the period or periods mentioned in the section only if the delay in disposing of the appeal is attributable to the assessee. The judgment of the Delhi High Court in Pepsi Foods (P.) Ltd. v. Asstt. CIT [2015] 57 taxmann.com 337/ 232 Taxman 78 (Delhi) affirmed.

DCIT Vs. Pepsi Foods Ltd [2021] 126 taxmann.com 69 (SC)

Dismissal of SLP against the order of the High Court where it was held that merely because cash deposits accepted were deposited in bank account the penalty u/s. 271D will not be levied

Director of the assessee company obtained loan/cash exceeding Rs. 20,000 from financier. Loans so obtained were deposited by him in cash in bank account of assessee company. In response to SCN, regarding violation of provisions of section 269SS, assessee explained that amount so received by director was deposited in company’s bank account on very same day and same was utilized to pay salaries, rents and EMI commitments. Thus, there was reasonable cause for having availed loan transactions in cash. Assessing Officer rejected assessee’s explanation and levied penalty u/s. 271D. The Madras High Court held that merely because director deposited cash obtained by it in the current account of assessee-company on very same day and assessee utilized it to pay salaries, rent and EMI commitments, same could not be a ground to be taken as a mitigating factor to escape from rigour of levy of penalty under section 271D. [Ref : Vasan Healthcare (P.) Ltd. v. Addl. CIT [2019] 103 taxmann.com 26 (Mad.)]. The SLP filed by the assessee against the judgment of the Madras High Court was dismissed by the Supreme Court holding that there was no reason to interfere in the matter.

Vasan Healthcare (P.) Ltd. Vs. Additional CIT [2021] 125 taxmann.com 266 (SC)

The Direct Tax Vivad se Vishwas Act, 2020 – Pending prosecution for unrelated issue – Eligibility to file the declaration under the Act

Where there was a pending prosecution for assessment year in question on an issue which was unrelated to tax arrear, holding that an assessee would not be eligible to file a declaration would defeat very purport and object of Vivad se Vishwas Act. Such an interpretation which abridges scope of settlement as contemplated under Vivad se Vishwas Act could not be accepted.

Macrotech Developers Ltd. v. Principal Commissioner of Income Tax - [2021] 126 taxmann.com 1 (Bombay)

Compensation for pre-mature termination of Lease Agreement held allowable as deduction u/s. 37(1) + Deduction of Bad Debts u/s. 36(1)(vii) for Debtors acquired in a slump sale transaction.

Issue I : Assessee terminated lease and licence in respect of two warehouses. The lesser deducted a sum of Rs. 45.16 lacs towards compensation for premature termination of lease agreement. The compensation so deducted amounting to Rs. 45.16 Lakhs was claimed as deduction. Assessing Officer disallowed assessee’s claim. However, the Tribunal held that early termination of lease was a business decision and expenditure incurred in relation to same was wholly and exclusively for purpose of business and allowed assessee’s claim. On department’s appeal to High Court, the High Court affirmed the decision of the Tribunal and allowed the claim of the assessee.

Issue II : Assessee purchased certain assets on slump sale basis and in process certain debts which were part of current assets were reduced. The assessee wrote off a sum of Rs. 1.76 crores claiming same as bad debts and eligible for deduction u/s. 36(1)(vii). The Assessing Officer and the CIT (A) denied the claim of the assessee for the reason that the assessee was claiming double benefit in respect of the same item. Once as a reduction from the cost of undertaking under slump sale and again as bad debts. Tribunal held that lower authorities had completely ignored fact that under Adjustment to Purchase price’ purchaser reassigned some debts amounting to Rs. 2.44 crores to assessee and assessee reduced same from purchase price. The Tribunal also held that the finding of lower authorities that debts were transferred as part of net current assets in slump rule and assessee would get double benefit if allowed deduction in respect of write off book debts were wrong and against facts of case. The Assessee had rightly written off debts and same were addressable under section 36(1)(vii). On department’s appeal to the High Court, it was held that the Tribunal was justified in its view and the claim of the assessee was allowable u/s. 36(1)(vii) of the Act.

Pr. CIT Vs. Lee & Murihead (P.) Ltd. [2020] 119 taxmann.com 499 (Bombay)

Notice for reassessment u/s. 148 cannot be issued merely for making fishing inquiries – permissible if there is a application of mind and satisfaction of the AO

Notice under section 148 is not permissible for mere verification or for a fishing inquiry. However, in a case where there was tangible material as on date in hands of Assessing Officer that assessee had received shareholders’ funds from shell companies, and Assessing Officer, after due application of mind, had recorded a satisfaction of his own that income had escaped assessment, reopening of assessment was justified

Navnidhi Dyeing And Printing Mills (P.) Ltd. v. Asst. CIT [2021] 125 taxmann.com 365 (Gujarat)

Dismissal of appeal for the reason of not filing E-Appeal held not valid

Commissioner (Appeals) could not reject an appeal filed by assessee on a technical ground that same was not ‘e-filed’ within period of limitation prescribed under circular no. 20/2016.

CIT Vs. A.A. Antony - [2021] 125 taxmann.com 170 (Madras)

Exemption u/s. 54 for the Investment made in the name of the wife of the assessee

Assessee sold a residential house and invested sale consideration in purchase of a plot of land for the construction of a new residential house. The investment in the plot of land was however made in the name of the wife of the assessee. The assessing officer denied the exemption u/s. 54 for the reason that the investment is not made in the name of the assessee. This was confirmed by the CIT (A). On appeal to the Tribunal, it was held that mere fact that investment in new property was made in name of his wife could not be a reason for disallowance of deduction under section 54 to the assessee

Shankar Lal Kumawat Vs. ITO [2021] 125 taxman.com 347 (Jaipur Trib.)

Incomes to be included for the computation of Book Profit for the purpose of section 40(b)(v) of the Income-tax Act for eligible Partners’ Remuneration

Assessee was engaged in the manufacturing of aromatic chemicals. The Assessing Officer noticed that the total income of assessee included dividend income, interest on deposit, interest on income-tax refund and interest on recurring deposit, which were covered under the head “Income from other sources”. AO held that that these incomes were not directly related to the business income, therefore these amounts were required to be ignored while computing the “book profit” for computation of remuneration admissible under section 40(b)(v). The assessing officer relied on Explanation 3 to section 40(b)(v) for the above contention. Accordingly the excess remuneration was added back to the total income of assessee. CIT(A) upheld the order passed by the assessing officer.

On further appeal, Tribunal eld that a bare reading of Explanation 3 of section 40(b) make it evident that selection of any head of income, more particularly of the head Profit or gain of business or profession, is nowhere required or envisaged by the Legislature. There is no warrant to select the head of income so far as the computation of the permissible amount of the remuneration under section 40(b) is concerned. As regards Explanation 3 to section 40(b), the Tribunal held that the assessing officer does not get jurisdiction to go behind the net profit shown in the Profit & Loss account except to the extent of the adjustments provided in Explanation 3. He is not empowered to decide the head under which the income is to be taxed. The net profit as shown is not to be allocated into different components. Thus, this income could not be excluded for purpose of working out book profit to ascertain the ceiling of the partner’s remuneration.

Mac Industries Vs. ITO (2021) 124 taxmann.com 570 (Surat Trib.)

CA. Hinesh Doshi, CA. Pramita Rathi

Deputy Commissioner of Income Tax, Circle -5 (2), Kolkata vs. M/s. Sisecam Flat Glass India Ltd. [TS-179-ITAT-2021(Kol)] dated 15th March, 2021

Facts:

- The assessee, a company, was engaged in the business of manufacturing & processing of float glass, mirror glass etc.

- During the course of assessment, AO disallowed certain expenses w.r.t loss on interest rate (hedging contract) and monitoring fees for non-deduction of TDS u/s. 40(a)(ia) of the Income Tax Act, 1961.

- The assessee filed an appeal before CIT (A) which granted relief in regard to the above disallowances.

- Aggrieved, the revenue filed an appeal before ITAT.

Issue:

Whether the expenses incurred for loss on interest rate (hedging contract) and monitoring fees would be disallowed for non-deduction of TDS?

Held:

- ITAT observed that the monitoring fees paid qualified as ‘interest’ both under Income Tax Act, 1961 as well as the DTAA between India and Germany.

- ITAT also held that the payment made in question was not liable to tax deduction in terms of the specific exemption granted under Article 11(3)(b) of the Indo-German DTAA.

- ITAT stated that no tax was required to be withheld u/s. 195 of the Act for the said expense and therefore the same was allowed as a deduction.

- Relying on the co-ordinate bench ruling in case of M/s. Mcleod Russel India Ltd, ITAT held that loss incurred on currency interest rate arrangements with Bank was non- speculative in nature and deductible from the profits of the business.

- Hence, ITAT ruled in favour of the assessee.

M/s. Altisource Business Solutions Private Limited vs. Asst. Commissioner of Income-tax, Circle 1 (2) (International Taxation) Bangalore [TS-184-ITAT-2021(Bang)] dated 17th March, 2021

Facts:

- The assessee, a private limited company, was engaged in providing contract software development and support services and information technology (IT) enabled services including data analysis, compilation and transmission of customized software to overseas affiliates.

- During the assessment proceedings, AO disallowed software expenses paid to non-residents by invoking the provisions of section 40(a)(ia) of the Income Tax Act, 1961 as the assessee had not withheld tax on said payments u/s 195 of the Act.

- Aggrieved, the assessee filed an appeal before ITAT.

Issue:

- Whether TDS was required to be deducted for software expenses?

Held:

- ITAT observed that the assessee had only purchased software, which was copyrighted article and there was no transfer of copyright, and therefore, in such cases, the same would not be treated as “royalty” under the respective tax treaty.

- ITAT noted that the end user could only use the computer programme by installing it in the computer hardware and would not be able to reproduce the same for sale or transfer.

- ITAT also observed that the licence granted imposed restrictions or conditions for the use of the computer software.

- Relying on SC ruling in Engineering Analysis Centre of Excellence Private Limited, ITAT stated that as per Article 12 of the DTAA, the distribution agreements/ End-User License Agreements would not create any interest or right in such distributors/end users, which would amount to the use of or right to use any copyright.

- ITAT held that the consideration paid to non-resident software manufactures / suppliers would not give rise to income taxable in India and, therefore was not liable for deduction of tax at source u/s 195 of the Act.

- Accordingly, ITAT ruled in favour of the assessee.

M/s. Sundaram Business Services Limited vs. Income Tax Officer, Corporate Ward 6(3), Chennai [TS-193-ITAT-2021(CHNY)] dated 19th March, 2021

Facts:

- The assessee, a company, was engaged in the business of providing IT enabled services, outsourcing services.

- The assessee paid professional charges to two offshore entities, a Chartered Accountant company and a law firm, for rendering professional services without deduction of tax at source on the grounds that professional charges paid to offshore entities did not come under the provisions of section 195 of the Income Tax Act, 1961.

- During the assessment proceedings, AO disallowed said expenses as AO opined that TDS was required to be deducted even though the payments were made to the offshore entities.

- Aggrieved, the assessee filed an appeal before ITAT.

Issue:

- Whether TDS was required to be withheld on payment made towards professional charges to offshore entities?

Held:

- ITAT stated that professional services rendered by an individual/ firm of individuals, being a resident of one of the Contracting States would be taxable only in that State unless individual or firm has a fixed base in India.

- ITAT noted that the professional services in relation to legal services were in the nature of independent professional services as defined under Article 14 of India-Australia DTAA and hence was outside the scope of definition of royalties as defined u/s.9(1)(vi) of the Act, and thus, outside the scope of provision of section 195 of the Act.

- ITAT, as regards to Chartered Accountancy Services, stated that even though the said payment was not covered under Article 14, it was covered under Article 7 of India-USA DTAA.

- ITAT observed that the Chartered Accountant company had no PE in India and also the services were rendered outside India.

- ITAT held that above service was, thus, outside the scope of provisions of section 195 of the Act, because it was neither in the nature of royalties as defined u/s.9(1)(vi) of the Act nor in the nature of fess for technical services because the nature of services rendered by the company of accountants did not make available technical knowledge, expertise, skill, know-how or processes to the assessee.

- Accordingly, ITAT ruled in favour of the assessee.

CA. Manoj Shah, CA. Atal Bhanja

RBI Notification No. RBI/2021-22/17 DOR.STR.REC. 4/21.04.048/2021-22 Dated April 7, 2021

Asset Classification and Income Recognition following the expiry of Covid-19 regulatory package

Refund/adjustment of ‘interest on interest’

All lending institutions1 shall immediately put in place a Board-approved policy to refund/adjust the ‘interest on interest’ charged to the borrowers during the moratorium period, i.e. March 1, 2020 to August 31, 2020 in conformity with the above judgement. Methodology for calculation of the amount to be refunded/adjusted for different facilities shall be finalised by the Indian Banks Association (IBA) in consultation with other industry participants/bodies, which shall be adopted by all lending institutions. The above reliefs shall be applicable to all borrowers, including those who had availed of working capital facilities during the moratorium period, irrespective of whether moratorium had been fully or partially availed, or not availed, in terms of the circulars DOR.No.BP.BC.47/21.04.048/2019-20 dated March 27, 2020 and DOR.No.BP.BC.71/21.04.048/2019-20 dated May 23, 2020 (“Covid-19 Regulatory Package”). Lending institutions shall disclose the aggregate amount to be refunded/adjusted in respect of their borrowers based on the above reliefs in their financial statements for the year ending March 31, 2021.

Asset Classification

Asset classification of borrower accounts by all lending institutions following the SC judgment shall continue to be governed by the extant instructions as clarified below.

- In respect of accounts which were not granted any moratorium in terms of the Covid19 Regulatory Package, asset classification shall be as per the criteria laid out in the Master Circular - Prudential norms on Income Recognition, Asset Classification and Provisioning pertaining to Advances dated July 1, 2015 or other relevant instructions as applicable to the specific category of lending institutions (IRAC Norms).

- In respect of accounts which were granted moratorium in terms of the Covid19 Regulatory Package, the asset classification for the period from March 1, 2020 to August 31, 2020 shall be governed in terms of the circular DOR.No.BP.BC.63/21.04.048/2019-20 dated April 17, 2020, read with circular DOR.No.BP.BC.71/21.04.048/2019-20 dated May 23, 2020. For the period commencing September 1, 2020, asset classification for all such accounts shall be as per the applicable IRAC Norms.

RBI Notification No. RBI/2021-22/20 DoR.LIC.REC.5/16.13.218/2021-22 Dated April 8, 2021

Enhancement of limit of maximum balance per customer at end of the day from ₹1 lakh to ₹2 lakh – Payments Banks (PBs) done with immediate effect.

RBI Notification No. RBI/2021-22/21 DOR.CRE.REC.06/04.02.001/2021-22 Dated April 12, 2021

Interest Equalization Scheme on Pre and Post Shipment Rupee Export Credit-Extension

Government of India has approved the extension of Interest Equalization Scheme for pre and post shipment Rupee export credit, with same scope and coverage, for three more months i.e., upto June 30, 2021. The extension takes effect from April 01, 2021 and ends on June 30, 2021 covering a period of three months. Consequently, the extant operational instructions issued by the Reserve Bank under the captioned Scheme shall continue to remain in force upto June 30, 2021.

RBI Notification No. RBI/2021-22/16 A.P. (DIR Series) Circular No. 01 Dated April 07, 2021

External Commercial Borrowings (ECB) Policy – Relaxation in the period of parking of unutilised ECB proceeds in term deposits

Unutilised ECB proceeds drawn down on or before March 01, 2020 can be parked in term deposits with AD Category-I banks in India prospectively for an additional period up to March 01, 2022. All other provisions of the ECB policy remain unchanged.

RBI Has issued some Master Circulars on 1st April 2021. Interested persons can visit the website https://www.rbi.org.in/scriptS/NotificationUser.aspx for further awareness on the said subject.

Investment by Foreign Portfolio Investors (FPI): Investment Limits

A.P. (DIR Series) Circular No. 14 dated March 31, 2021

a. Investment Limits for FY 2021-22 a. The limits for FPI investment in Corporate bonds shall remain unchanged at 15% of outstanding stock of securities for FY 2021-22. Accordingly, the revised limits for FPI investment in corporate bonds, after rounding off, shall be as under (Table - 1)

|

Table - 1: Limits for FPI investment in Corporate bonds for FY 2021-22 |

|

|

(₹ Crore) |

|

|

Current FPI limit |

5,41,488 |

|

Revised limit for HY Apr 2021-Sep 2021 |

5,74,263 |

|

Revised limit for HY Oct 2021-Mar 2022 |

6,07,039 |

b. The revised limits for FPI investment in Central Government securities (G-secs) and State Development Loans (SDLs) for FY 2021-22 will be advised separately. Till such announcement, the current limits (as in Table - 2), shall continue to be applicable.

|

Table - 2: Limits for FPI investments in G-Sec and SDL |

||||

|

(₹ Crore) |

||||

|

G-Sec General |

G-Sec Long Term |

SDL General |

SDL Long Term |

|

|

FPI investment limits |

2,34,531 |

1,03,531 |

67,630 |

7,100 |

FETERS – Cards: Monthly Reporting

A.P. (DIR Series) Circular No. 13 dated March 25, 2021